Shake Shack is filing for an IPO.

This should be welcome news to all burger aficionados out there. It also made me think a bit about the comparison to high-flying tech companies. Sometimes, a reality check comes in handy and the company’s filing at a supposed USD 1bn valuation shows a remarkable similarity to any turbo-charged tech company success story. Despite not being tech at all.

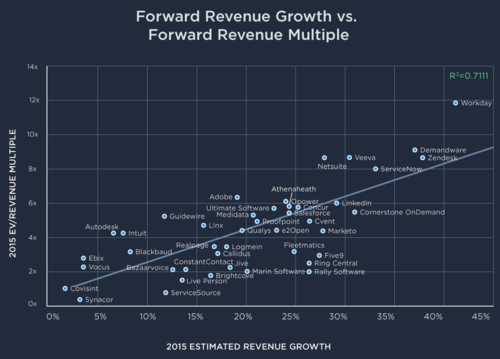

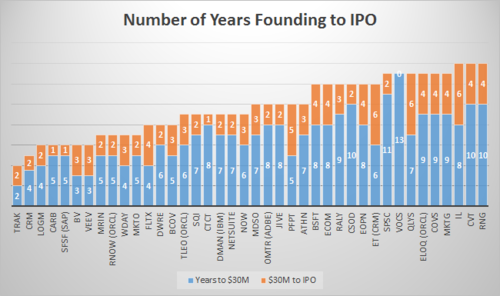

Granted, the investment inflow into Shake Shack will presumably have been higher than your average software play. But on all other accounts, its key IPO metrics are on par with any SaaS filing, and largely outperform anything in the ecommerce world. With its 2013 revenue run rate, it will be valued at a revenue multiple of 8.5 to 9, and will have filed for IPO within 10 years. This is perfectly in line with most SaaS ‘unicorns’ that went public in the last ten years:

What does this tell us? Foremost, it puts the “tech trumps everything” theme a little bit in perspective.

Yes, cloud technology companies operate at incredible capital efficiency and enjoy exponential distribution capabilities, riding the wave of the digital revolution. Nevertheless, the burger joints in extremely competitive – and to a technologist seemingly undifferentiated – markets can come up with similar success stories. That is if they show strong growth and a healthy profit contribution structure. Shake Shack does and demonstrates it through its ”shack-level operating profit margin”. Markets will reward these factors in any industry.

Lastly, it also confirms the notion that revenue growth is the single determinant of IPO valuations, be it in software or beef patty “hardware”: