There is little doubt that financial markets have been particularly nervous lately, especially regarding the European banking sector (once again!).

Clearly, the Brexit vote on the 23rd of June has been the reason that reignited such worries. Now, it is more likely to lead to weaker economic growth in Europe and possibly to lower interest rates. The combination of these two factors is not good news for banks as it might result in lower profits and more bad loans.

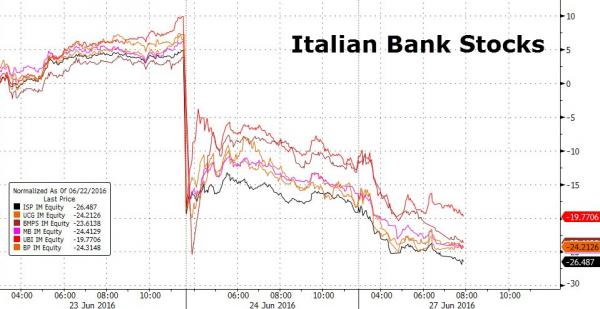

However, apart from Brexit, there is another potentially larger worry for the markets and that is none other than the banking sector in Italy. As The Economist put it, “The shockwaves from Brexit have been almost as severe on the Tiber as on the Thames”.

Bad loans approaching one fifth of the GDP

Bad loans approaching one fifth of the GDP

Italy is Europe’s 4th largest economy but it is currently one of its weakest.

It has high public debt and high unemployment and its banks appear to be facing severe problems with bad loans approaching one fifth of total gross loans, which is also approximately one fifth of the country’s GDP. The bank facing the worst troubles of the lot is Monte dei Paschi di Sienna, the world’s oldest bank (founded in 1472).

It is worth pointing out that recently, the European Central Bank asked the bank to reduce its bad loan tally substantially. The troubles of the bank have been reflected in its share price where, as can be seen from the chart above, it lost 46% of its value since Brexit.

Italian banks likely to turn to the government …

Clearly then, Italian banks will need to put their balance sheets in order, but to do that they will require vast amounts of capital.

As we have learnt in the past few years this is no easy task, especially given the recent share price performance of Italian banks, which has caused foreign investors to sell their shares and move on.

As such, with private capital difficult to attract, it is very likely that a number of banks will turn to their government for support (like so many others in the Eurozone did in the past). This is where things get complicated because new Eurozone rules regarding government support state that a bank cannot receive such support unless its junior bondholders take losses first, the so-called “bail-in” principle.

And this is where the catch is. In most countries, junior bonds are held by large institutional investors, such as insurance and pension funds. It is assumed that they are sophisticated enough and understand the various risks that they face. In the case of Italy, a large part of such bonds (around 200 billion Euros!) is held by millions of retail investors, who acted as if they were “depositing” and not “investing” their money.

Actually, there have been many voices in the EU arguing that retail investors should be excluded from the new “bail-in” rules.

… But the “bail-in” principle is likely to hurt Italy and the EU!

Now, here the situation becomes even more complicated. Because, if the Italian government “forces” millions of small retail investors to take losses on their bond holdings in the banks, the political cost is going to be huge. Italians will feel hard done because, before the new rules were enacted, a large number of countries in the European Union poured billions of Euros (that is to say taxpayers’ money) to “bail-out” their banks.

And this dissatisfaction would come at a very bad point in time, too, as it would mean that a large portion of the Italian population will lose faith in the Eurozone. It could also prove very costly for Matteo Renzi, the Italian prime minister, who is running a referendum for reforming the constitution in the coming autumn.

The EU faces a dilemma

So how does the European Union handle the Italian situation? Well, it faces a very challenging dilemma.

On one hand, there are the “bail-in” rules, which are being put to the test for the first time. While on the other hand, there is a potential banking (and not only) crisis emerging in one of its largest and founding states. And all this is happening a few weeks after Brexit!

Whatever the case and the politics (e.g. Brussels vs. local), one thing is for sure: confidence needs to be restored in the Italian banking system.

Otherwise, we are going to witness a further deterioration of the situation, which would be particularly bad news for the fragile European and global economies. How will this be done will depend on each case; some banks might be in a position to raise private capital (the healthier ones), others might eventually need to go to the government.

In addition, it is possible that we will also witness a broader restructuring of Italy’s banking system which is likely to involve asset sales and consolidation of smaller banks.

What do you think? Will the Italian banking sector resolve the current woes? Share your thoughts in the comments’ section below.

For more finance tips, check our finance section and subscribe to our weekly newsletters.